China on Friday sold 30-year treasury bonds as part of a massive 1 trillion yuan (US$138 billion) sale of ultra-long bonds aimed at supporting the world’s second-biggest economy at a time when local government coffers have been drained by the pandemic and by the collapse of the real estate bubble, state media reported.

The funds – which include sales of 50-year bonds next month – will raise money for "major national strategies" including technological innovation, food and energy security and a nationwide program to tackle the aging population, which is projected to steadily decline.

Beneficiaries will include cash-strapped local governments and high-tech companies, an investment manager in a southern Chinese city who declined to be identified for fear of reprisals.

China's finance ministry warned local governments in January 2023 that there wouldn't be any straight-up bailouts from the central government in Beijing.

But now, governments and state-owned companies at provincial, city and county level will be able to apply for targeted funding from the central government to meet the cost of nationwide policies decided in Beijing, the investment manager said.

"Our clients will be getting notices from local governments, asking them to fill out forms if they wish to apply for national bond funds," the manager said. "The funds are available to cover a wide range of activities, including public projects and cutting-edge technology companies."

Coupon of 2.57%

All told, there will be 22 bond sales through mid-November: Seven sales of the 20-year bonds, 12 issuances of 30-year bonds, and three issuances of 50-year bonds.

On Friday, bidding started for the first tranche of 30-year bonds worth 40 billion yuan. The coupon rate was 2.57%; interest will be paid semiannually.

The 20-year bonds will be issued first on May 24, and the 50-year ultra-long bonds will go on sale on June 14.

According to the state-run China Daily newspaper, some of the funds raised will be used to improve urban drainage following disastrous flash floods in recent years, upgrade the education and healthcare systems and improve transportation infrastructure.

They will also be used for "high-quality population development," a reference to attempts to boost the flagging birth rate and tackle population aging.

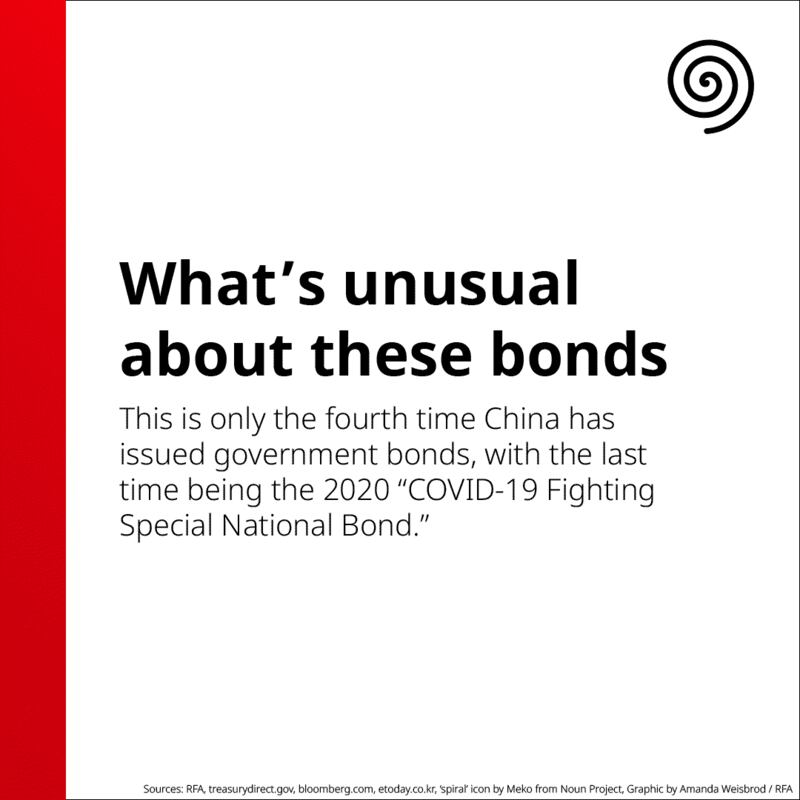

The last big issuance of 1 trillion yuan in government debt was in October 2023; the latest is described as "special," although it is one among a number of similar issuances planned for the next few years by Premier Li Qiang.

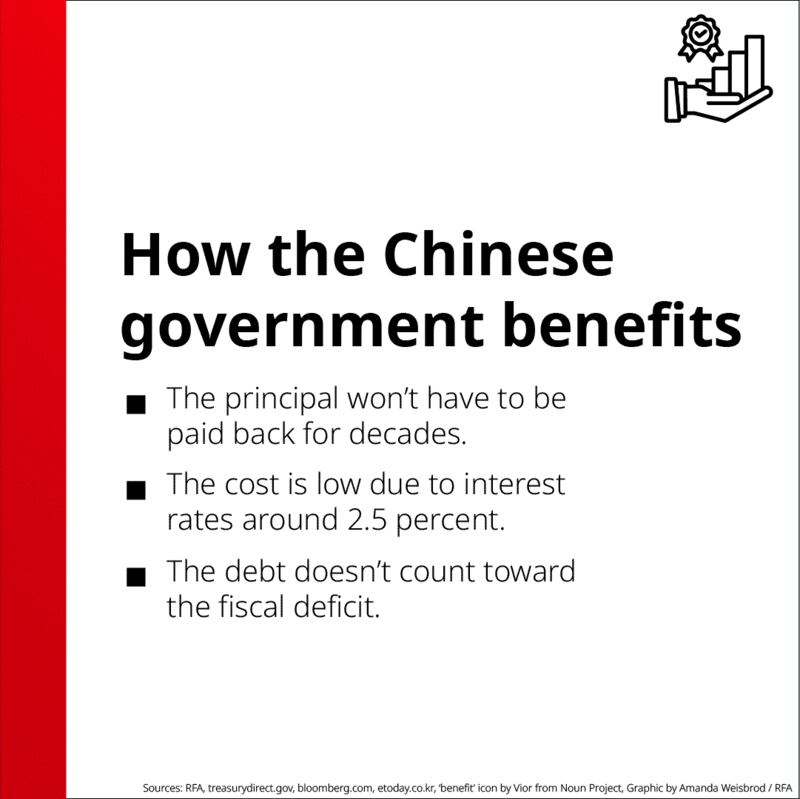

One of the benefits to the government of bond issuances is that they don't count towards its fiscal deficit, which is officially supposed to remain below 5% of GDP, according to U.S.-based economist Cheng Nong.

"The Chinese local government debt problem is getting more and more serious, and the central government's fiscal revenue deficit from taxation is very large," Cheng said. "Increasing the fiscal deficit would violate the law that the fiscal deficit can't exceed 5% of GDP."

"If they broke through that threshold it would be very damaging for the image of the Chinese Communist Party," he said, adding that administering the funds in this way allows a greater degree of control by the central government over how they are spent.

According to the investment manager, local governments and enterprises can apply for a range of different kinds of funding, depending on the policy being implemented.

"Many are low-interest or interest-free loans, and some are in the form of subsidies," he said.

Times of hardship

The Chinese government has typically resorted to issuing special government bonds at times of economic hardship, selling 270 billion yuan of bonds during the Asian financial crisis in 1998, 1.55 trillion during the subprime mortgage crisis of 2007 and 1 trillion at the start of the COVID-19 pandemic in 2020, according to Zhang Jie, a former branch manager at a Chinese commercial bank.

In the absence of a rebound in consumer spending and growing barriers to exports amid a trade war with the United States and growing concern in Europe, government investment is the only route left for the current administration to stimulate growth, Zhang said.

Cheng Cheng-ping, professor of finance and banking at Taiwan's Yunlin University of Science and Technology in Taiwan, said the strategy is a good one for Beijing, at a time when interest rates are very low.

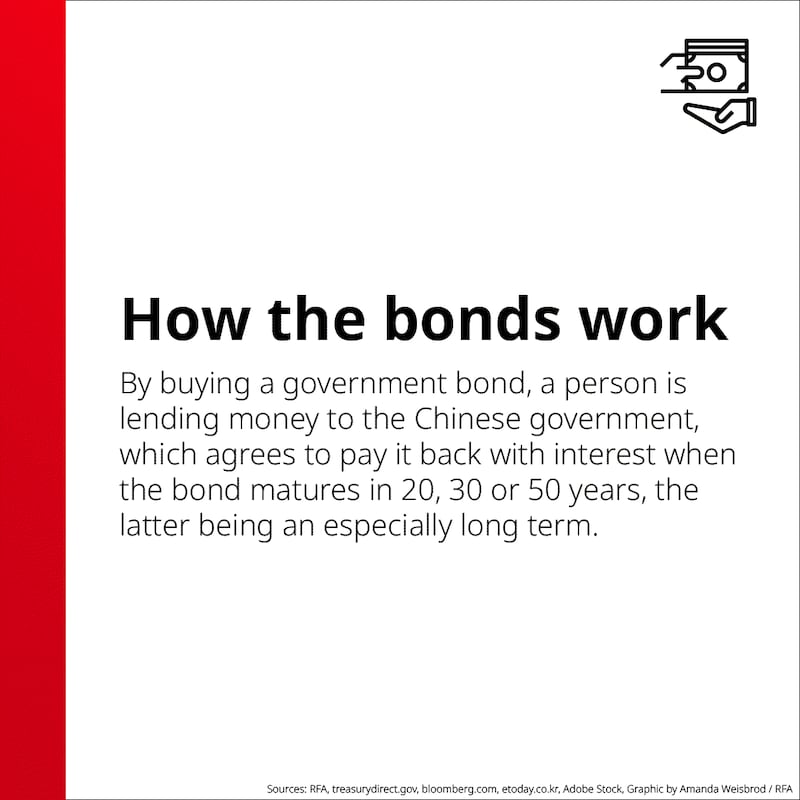

"This carries a lot of benefits for the Chinese government; they don't need to pay back the principal for 20, 30 or 50 years, and the cost of issuing treasury bonds is low due to the current low interest rates," he said. "There are many benefits when it comes to stimulating supply and demand."

The bonds aren't being marketed to the general public, however, and will likely mostly be traded among financial institutions, a former bank employee from Shanghai who asked not to be identified told Radio Free Asia.

"They're mostly sold to banks to offset the high deposit in China," he said, adding that people are leaving their money in the bank rather than spending it. "[The banks] have too much money to lend out, so they buy these long-term treasury bonds."

"They're for interbank circulation and may not be so easy for individual buyers to trade," the man said. "I won't be buying them, at any rate. It's hard to say if I will even be around in 50 years."

Translated by Luisetta Mudie. Edited by Malcolm Foster.